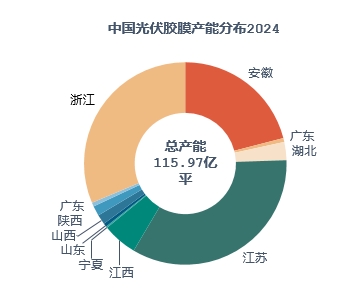

By the end of 2024, China's total PV film capacity is expected to reach approximately 11.6 billion m², up 35% YoY. Despite the capacity growth, the capacity utilisation rate in 2024 is projected to decline from 52.1% to 44.49%. Although China's technological advantages and cost control have further solidified its position in the global PV film market, the low industry entry barriers and increasing module production have led to continuous capacity expansion. This has intensified competition and driven prices downward. Under strict cost control for modules and the weaker bargaining power of film suppliers, PV film prices have remained inverted, exacerbating cash flow pressure. High-cost capacity is expected to gradually exit the market from 2024 to 2026.

According to SMM statistics, the 2024 shipment volumes of the top 10 PV film enterprises (including overseas shipments) are as follows:

Overall, the 2024 production has reached 5.424 billion m², up 10.4% YoY. The top 3 producers accounted for 3.5 billion m², with a market share of 69.4%. The PV film industry is showing a trend where large enterprises are expanding while smaller ones are shrinking and exiting the market.

In Q4, Swick's shipments increased rapidly, up 28.83% QoQ compared to Q3, demonstrating strong growth potential.

![[SMM PV News] Swift Solar Acquires Meyer Burger Assets to Build US Tandem Cell Gigafactory](https://imgqn.smm.cn/usercenter/fYlYx20251217171740.jpg)